Investment market performance Q4 2025

As we navigate the complexities of the financial landscape, it’s important to stay informed about how investment markets are performing. The fourth quarter of 2025 (October 1 – December 31) presented both challenges and opportunities for investors. In this article, we take a closer look at how investment markets performed over the quarter, and we highlight some of the key economic factors from across the world, that influenced these outcomes.

Australia

Share market: The Solactive Australia 200 Index, which represents Australia’s top 200 companies, was down -1.0% over the quarter. Positive returns from the mining sector, including companies such as Rio Tinto and Fortescue, were offset by negative performance from Technology, Health Technology, Finance and Retail companies.

Interest rates: Australia’s inflation rate rose to 3.8% in Q4 2025, up from 3.4% in Q3 and was above the Reserve Bank of Australia’s (RBA) target range of 2-3%. Core inflation, which excludes volatile items like food and energy, rose from 3.0% in Q3 to 3.4% in Q4 2025. The RBA kept the cash rate at 3.60% through Q4 after lowering it from 3.85% in August. Following the hotter-than-expected inflation numbers, markets are no longer expecting any further rate cuts in this cycle, but are instead expecting possible rate hikes in early 2026.

Housing market: The Australian housing market, as measured by Cotality's Home Value Index (HVI), recorded an increase of +2.7% in Q4 2025, following a similar +2.7% increase in Q3 2025. The increase over the whole of 2025 was +8.3%. The strong growth in 2025 has been attributed to a combination of factors that include housing supply shortages, population growth driven by immigration,along with falling interest rates, which have acted as a catalyst for renewed momentum.

Australian dollar: The Australian dollar (AUD) continued to recover against the US dollar over the quarter, rising 0.6% from 66.1 to 66.7 cents. The continued recovery is due to factors such as improved global risk sentiment, along with stronger inflation and economic data in Australia that has substantially reduced the chance of further interest rate cuts in Australia.

New Zealand

Share market: The Solactive New Zealand Top 50 Index saw a +2.1% rise in Q4 2025, with the positive return due to strong performance in Auckland International Airport and the a2 Milk Company, a leading exporter of milk-related products.

Housing market: The QV House Price Index showed no change in house prices nationally in the three months to the end of November 2025. House prices are now 0.1% higher than the same time in 2024, and 13.4% below the market peak in January 2022. The average property value nationally is now NZ$907,274.

Interest rates: The official cash rate was reduced from 3.0% to 2.5% in October 2025, with another cut to 2.25% in November 2025. It appears likely that this marks the bottom of the interest rate cycle for New Zealand, with the next move possibly being a hike sometime in 2026 depending on future inflation results. New Zealand’s economy, which saw a contraction in Q2 2025 of -1.0%, saw an increase of 1.1% in Q3 2025. Inflation was 3.0% in Q3 2025, slightly higher than the 2.7% recorded in Q2.

United States

Share market: US stocks had a modestly positive quarter, although they lagged international stock markets. The US stock market was held back by the record-long US government shutdown, rising job cuts and weakening consumer confidence.

Interest rates: The Federal Reserve cut interest rates from 4.25% to 3.75% in Q4 2025. This is in line with the Fed’s goals of achieving maximum employment and price stability. The Personal Consumption Expenditures (PCE) inflation rate stood at +2.8% at the end of September, while core inflation was at 2.6% at the end of November 2025.

A review of 2025

Financial markets saw continued positive returns through Q4 2025, rounding off a year of strong positive returns across all major asset classes. The strong returns of 2025 came about despite a stream of negative news, geopolitical and economic uncertainty and trade tensions. While US stocks saw strong performance through 2025, International stock markets and Emerging Market stock markets in particular saw very strong returns throughout the year, with Emerging Markets rising over 20%. Bond returns were positive through the year, although more muted than stock market returns.

We continue to monitor the major drivers of markets and their impact on Resolution Life Australasian portfolios. While investing always involves managing uncertainty, the current environment is mired in elevated uncertainty. The best form of defence for portfolios is to continue to be well diversified, with exposure to a range of asset classes that can help during volatile times.

Sources:

1. Solactive Australia 200 Index Performance - Solactive

2. Solactive New Zealand Top 50 Index Performance – Solactive

3. Reserve Bank of Australia Monetary Policy - RBA

4. Reserve Bank of New Zealand Official Cash Rate - RBNZ

5. Australian House Prices – CoreLogic Home Value Index

6. NZ house Prices – QV House Price Index

7. FactSet

8. Trading Economics

Helping your clients stay covered: 2026 reinstatement rule updates

Refining the reinstatement process: Updates to the 30-day grace period

At Resolution Life, we are committed to providing you with the latest information to help manage your clients' cover. We’ve recently updated our 30-day grace period reinstatement rules for Elevate, RPP, AC&L, FLP, CrisisCare, and TLI products.

These updates simplify the eligibility criteria, making it easier for you to help clients restore their protection if a policy lapses due to non-payment.

What is changing?

We’ve refined the logic behind our reinstatement process to provide more flexibility and clearer timelines:

- Clarified timelines: The 30-day grace period now officially begins from the date that the lapse cancellation/confirmation letter is sent, giving you a definitive window of time to act.

- Increased flexibility for past lapses: Previously, a policy could not be reinstated if it had lapsed previously in the last 12 months period. We’ve now expanded this: customers are now eligible if you they had no more than one lapse in the previous 24 months.

- Claims history: To be eligible for reinstatement, there must not have been any claims made on the policy within the 12 months immediately preceding the lapse.

Eligibility checklist

To reinstate the policy within this 30-day window without providing new health evidence, the following must apply:

- Payment: All outstanding premiums must be paid in full.

- Reason: The lapse must be due to non-payment (not a client requested cancellation).

- Duration: You must contact us and pay within 30 days of the lapse confirmation letter.

- History: No more than one lapse has occurred in the previous 24 months.

- Claims: No claims have been made on the policy within the 12 months preceding the lapse.

- Exclusions: Please note that n "Lifetime Benefit Period" Income Protection policies remain excluded from this specific 30-day reinstatement process.

Let’s work together

We want to ensure your clients stay protected. If you receive a lapse notification for a client, please reach out to us early. Our team is ready to help you navigate these new criteria and help you ensure your clients' coverage remains secure.

New streamlined Insurance transfer rules: Upgrading to Elevate

Streamlining cover transfers to the Elevate suite

We recognise that professional advice is the cornerstone of sustainable insurance outcomes. To support your practice, we have refined our internal transfer rules to provide you with a more efficient framework for managing your clients’ portfolios. These enhancements are designed to help you proactively transition clients from existing products into our modern Elevate suite, with significantly less friction.

Specifically, we have streamlined the migration pathways for both Lump Sum and Income Protection cover. By removing the traditional hurdles of new medical underwriting and extensive paperwork for "like-for-like" transfers, we are enabling a long-term retention strategy that allows you to modernise your clients' protection, while preserving their existing health insurability.

Why consider a transfer?

The insurance landscape has shifted significantly over the past decade. By transitioning to the Elevate suite, your clients can gain access to an insurance product designed for long-term sustainability. Whether they hold Lump Sum cover (Death, TPD, or Trauma) or Income Protection, we’ve removed the traditional hurdles to make staying protected simpler than ever.

What these changes mean:

We have updated our internal rules to ensure that eligible customers can move to Elevate with several key advantages:

- No new medical underwriting: For eligible "like-for-like" transfers (same or lesser sum insured), the requirement for fresh medical exams, blood tests, or health questionnaires has been waived.

- Seamless transition: All existing loadings and exclusions will automatically carry over to the new Elevate policy, preserving the client’s original underwriting terms.

- Income Protection: Clients can now transition into the Elevate Income Insurance Essentials product (IDII compliant). Benefit amounts are determined as the lesser of current cover or 70% of 1-year pre-claim earnings.

For a high-level summary of the transfer rules, view the Insurance Transfer Rules Flyer.

How to get started

To support your ongoing service, we have integrated these streamlined transfers into our Elevate remuneration structure. While the simplified, adviser-led process attracts 0% initial commission, it secures a long-term renewal stream of over 20%. For a detailed view of the rates and to discuss the flexibility of dialling renewals to nil—reach out to our team today.

Helping clients understand the value of insurance

Launched in December, the Value of Insurance campaign email will be sent to clients five months prior to their renewal date. This campaign complements our existing lifestage campaigns. It will specifically highlight why their insurance matters and encourages customers to reflect on their needs, reminding them also that their cover is flexible and to reach out to their adviser, if they need more information. You can view a sample here.

Improvement are being made to customers' annual statements

Why are changes being made?

To enhance customer experience and better educate customers about their cover (in an effort to reduce complaints and IDR/EDR/AFCA disputes), we want to provide earlier notification of any significant changes to their policy. This would give customers sufficient time to understand any impact and make informed decisions. This may include reaching out to their adviser to explore alternative options. By notifying customers earlier we have a better chance of retaining them or them taking advantage of continuation or conversion options.

Examples include:

- Changes to the criteria where customers can claim at certain policy ages (e.g. trauma cover being limited to Loss of Independence from a specified age, or a reduced percentage payable under a lifetime sickness benefit period after age 56).

- Changes to a customer’s cover following a change in occupation and/or periods of unemployment (e.g. loss or alteration of cover for Owner/Driver IP due to an occupation change).

- Adjustments to the customer’s premium structure (e.g. level premiums automatically switching to stepped premiums at a designated switch age).

- Cover ceasing at a specified age without clear communication of available conversion or continuation options (e.g. expiry of a Child Trauma option).

Although the terms of cover and premiums may change over time, customers are not currently provided with adequate education or advance notice of these changes. Additionally, the labelling or naming of the cover may remain the same, even where the underlying features or conditions have changed (e.g. cover still showing as “Trauma” after age 70, even though only Loss of Capacity applies). The plan over the next few quarters is to roll out a series of improvements and this email is about the release of the first tranche of changes.

When will the changes be implemented?

The Product team is pleased to confirm that the initial set of changes to the Insurance Schedules went live on Thursday, 5 March 2026.

Which Products are part of this release?

These updates will apply to all policies that include an Elevate, AC&L or Risk Protection Income Protection Plan. Plans impacted by this change are:

- Elevate Income Insurance Essentials

- Elevate Income Insurance Plan / Plus Plan

- Comprehensive Income Protection Plan

- Professional Income protection Plan

- Vital Income Protection Plan

- Essential Income Protection Plan

- Indexed Income Protection Plan

- Standard Income Protection Plan

- Premier Blue Ribbon Income Protection Plan

- Income Protection- Essential / Premier Plan

- Professional Income Replacement Plan

- Healthguard Income Protection Plan

- Reviewable Essential Income Protection Plan

- Securityguard Income Protection Plan

What are the details of the 4 changes in this release?

There were four separate concerns we addressed in this change:

- Clarification that payments cease the earlier of benefit period or policy expiry date.

Why change? A recent AFCA ruling against Resolution Life required the payment of benefits beyond the expiry age due to unclear disclosure. The Determination centres on when the customer’s 60 month IP benefit period ends while on claim, whether after 60 months or at policy expiry. Our position is that benefits cease at the earlier of the 60 month benefit period or the policy expiry date. AFCA also found the current schedule format unclear regarding when benefits end, noting that the benefit period shown does not reduce when a customer is on claim. In this case, the schedule still displayed a 60 month benefit period even though only 48 months remained until policy expiry, leading the customer to reasonably expect payments for the full 60 months.

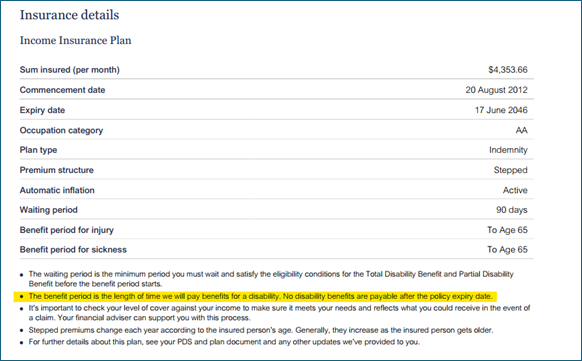

What is the change? To address this issue, all Income Protection Plans (except those with lifetime benefit periods) will now include the following disclosure on the insurance schedules/statements in the “Insurance details” section:

“The benefit period is the length of time we will pay benefits for a disability. No disability benefits are payable after the policy expiry date”

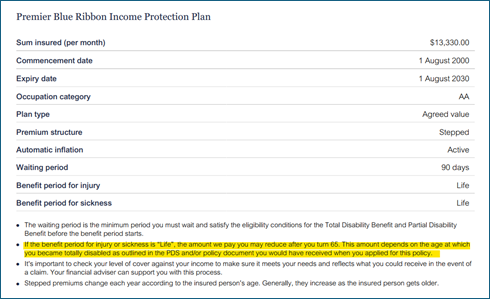

- Clarification for Lifetime Benefit periods that claim amount payable after Age 65 may be reduced.

Why change? A number of AFCA complaints have been received regarding the application of the sliding scale on Income Protection plans with a lifetime benefit period. Lifetime benefit periods were offered on AC&L and RiskPro Income Protection plans up until January 2002. It was available for both injury and sickness benefit periods. Customers could also have a combination of benefit periods. For example, they could have Lifetime benefit for Injury and a 5 year benefit period for sickness (only the sickness benefit could be less than lifetime, if a Lifetime benefit period was selected). Although the terms varied slightly between the AC&L and RiskPro plans, both included a sliding scale that applied once the life insured reached age 65.

What is the change? To address this issue, all Lifetime benefit Income Protection Plans will now include the following disclosure on the insurance schedules/statements in the “Insurance details” section:

“If the benefit period for injury or sickness is “Life”, the amount we pay you may reduce after you turn 65. This amount depends on the age at which you became totally disabled as outlined in the PDS and/or policy document you would have received when you applied for this policy.”

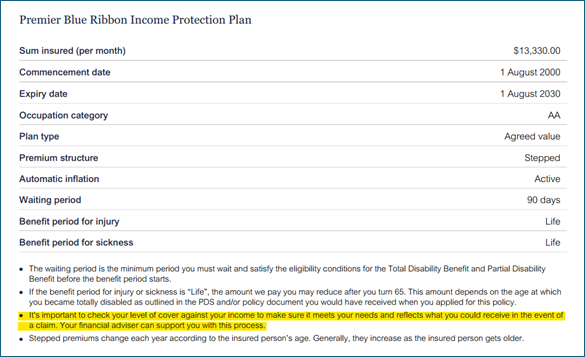

- Reminder for IP that amount of cover may not reflect current income levels.

Why change? There have been concerns that customers may be paying for benefits they cannot claim on due to over-insurance.

What is the change? To address this issue, all Income Protection Plans will now include the following disclosure on the insurance schedules/statements in the “Insurance details” section:

“It's important to check your level of cover against your income to make sure it meets your needs and reflects what you could receive in the event of a claim. Your financial adviser can support you with this process”

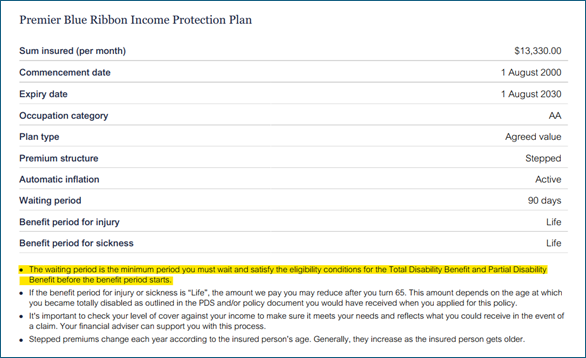

- Education around what waiting period represents.

Why change and what is the change?

No concerns have been raised regarding waiting periods. Nonetheless, we have proactively provided additional clarification on these. All Income Protection Plans will now include the following disclosure on the insurance schedules/statements in the “Insurance details” section:

“The waiting period is the minimum period you must wait and satisfy the eligibility conditions for the Total Disability Benefit and Partial Disability Benefit before the benefit period starts.”

We expect that customers may have more questions about Lifetime benefit period plans, particularly how they apply after age 65. Because these plans can be complex, we recommend directing enquiries to Customer Solutions or the customer’s Financial Adviser for guidance.

Important information

Where the information on this website is factual information only, it does not contain any financial product advice or make any recommendations about a financial product or service being right for you. Any advice is provided by Resolution Life Australasia Limited ABN 84 079 300 379, AFSL No. 233671 (Resolution Life), is general advice and does not take into account your objectives, financial situation or needs. Before acting on this advice, you should consider the appropriateness of the advice having regard to your objectives, financial situation and needs, as well as the product disclosure statement and policy document for the product. Any guarantee offered in the product is only provided by Resolution Life. Any Target Market Determinations for our products can be found at resolutionlife.com.au/target-market-determinations.

Resolution Life does not make any representation or warranty as to the accuracy, reliability or completeness of material on this website nor accepts any liability or responsibility for any acts or decisions based on such information.

The contact details for Resolution Life can be found at resolutionlife.com.au/contact-us.